Using ETFs in an Absolute Return Portfolio

In this environment of global economic uncertainty, many sophisticated investors and portfolio managers turn to “absolute return” strategies in an effort to make money under any market conditions … not to mention reduce their stress levels. This generally involves both long and short baskets of stocks, seeking to capture the performance spread between them, and a solid relative ranking system can make this a successful strategy.

But many investors and portfolio managers shy away from shorting individual stocks, and even put options have their drawbacks. One alternative that is growing in its appeal is the use of exchange-traded funds (ETFs) within an absolute return strategy.

Absolute Return as a Portfolio Strategy

Click here to order your copy of The VXX Trend Following Strategy today and be one of the very first traders to utilize these unique strategies. This guidebook will make you a better, more powerful trader.

Absolute return is the actual return that an asset or portfolio of assets achieve over time, without regard to how it performs relative to a benchmark (i.e., relative return). An absolute return strategy strives for positive returns in all market conditions, whether the market goes up or down – usually by implementing some form of market neutral, long/short, or hedged approach, employing short selling, futures, or options. The resulting portfolio is expected to show low correlation with the overall market.

Limiting Risk

Here’s a quick review of the risks traders must address. Keep in mind; you can’t make any kind of meaningful return without taking on some risk. There are two kinds of risk that we deal with in the stock market: systematic and unsystematic.

Unsystematic risk is company or industry-specific risk. It is also known as specific, diversifiable, or residual risk. It can be reduced through diversification. The impact from a bad news event, an earnings miss, or an analyst downgrade is considered unsystematic risk.

But you can’t diversify away all risk. Systematic risk is also known as market risk or un-diversifiable risk. It represents the risk inherent to the entire market or an entire market segment. The impact from things like global recession, war, terrorism, or inflation cannot be reduced or controlled through diversification, but it can be addressed through hedging.

The way we limit unsystematic risk in an absolute return strategy is to diversify by buying “baskets” of longs and shorts so that one or two blow-ups won’t destroy your entire portfolio. Equity ETFs are by definition baskets of stocks, so they offer an easy way to diversify a portfolio in a single investment.

To address systematic or market risk, you must hold positions that move opposite to your long positions. Ideally, the investments you select for a short portfolio will underperform those you selected for your long portfolio, and you capture the positive performance spread in either an up or down market.

The drawbacks to shorting stocks include unlimited risk if a stock moves against you and uncertainty in the availability of shares to borrow. And although purchasing put options will limit your financial risk to the premium paid (i.e. purchase price), it often will also limit your ability to fully participate in the stock’s movement depending upon things like changes in implied volatility (vega), time premium erosion (theta), leverage achieved (lambda), or option expiration before the anticipated move in the stock occurs.

Using ETFs in an Absolute Return Strategy

An alternative that is gaining popularity is to trade ETFs rather than individual stocks or options. Unless thinly traded, most ETFs are easily shorted and usually optionable, and often there are inverse ETFs available that the trader can buy long while achieving the same performance as a short position.

Once you have selected an appropriate ETF relative ranking system, there are different ways to trade it. Many portfolio managers employ a long-only sector rotation strategy in which they buy long the top 2-4 sectors from the ranking system, and perhaps weight positions in accordance with their relative scores. They then change the portfolio composition, either on a set schedule or whenever the rankings change significantly.

However, for those who don’t want to bet on which way the market is going, a long/short absolute return approach makes sense – that is, go long the 2-3 top-ranked ETFs and short the 2-3 lowest-ranked ETFs.

Also worth mentioning is a more aggressive strategy in which you trade some of the highest and lowest ranked stocks from within those top and bottom-ranked ETFs to further juice returns. This would be considered an enhanced ETF long/short strategy.

Example of an Absolute Return Long/Short ETF Strategy

Sabrient has developed a robust, fundamentals-based, quantitative stock evaluation model that we have found to be particularly effective for absolute return long/short strategies. It scores stocks based on growth projections, projected valuation, historical return ratios, and earnings quality, with a one-month forward outlook. We call it the Company Outlook Rank. Over time, our testing has shown that the highest-scoring stocks tend to greatly outperform the lowest-scoring stocks.

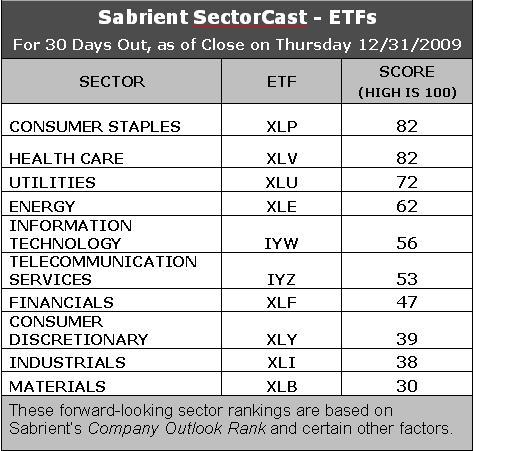

We can use this model to evaluate individual stocks, and then build bottom-up profiles of the ETFs based on their appropriately weighted stock constituents. The result is a quantitative sector ranking model called SectorCast. On the right is a table of the relative rankings, as of December 31, of the ten primary S&P GICS sectors, using the sector ETFs shown as proxies.

The clear leaders in this instance were Consumer Staples and Health Care, followed by Utilities, which put a definite conservative bent to the rankings at year end after a prolonged market rally. Note that the more economically sensitive sectors of Materials, Industrials, Consumer Discretionary, and Financials were at the bottom of the rankings. In effect, the rankings were recommending a long/short portfolio positioned for a market pullback sometime during the ensuing month, which is indeed what occurred.

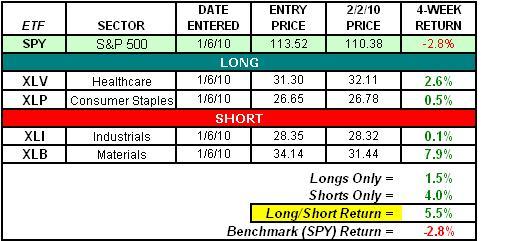

Below is a table showing the long/short ETF portfolio for an absolute return strategy based on these rankings. We bought the top two ETFs in equal weights with all allocated cash, and shorted the bottom two ETFs in equal weights against the margin provided by the long positions. This model portfolio is published each week in our Sector Detector blog post. Also shown is what a comparable long investment in the ^SPY^ would have returned.

As it turned out, it was a particularly productive month for implementing an absolute return ETF strategy. The entries assumed the opening prices on Wednesday morning, January 6. Four weeks later, after a significant market pullback, the SPY was down -2.8%, but the absolute return portfolio was up a robust +5.5%. Best of all, each of the four positions was making money, with the two long positions averaging +1.5% and the two short positions averaging +4.0% returns.

As you can see, the short position in Materials was the best performer (+7.9%), as our fundamentals-based model was screaming that the strength in Materials was driven more by technicals and sentiment than fundamentals, perhaps due to expectations of inflation and further weakness in the dollar.

This example illustrates the ideal outcome for a long/short strategy. Of course, it doesn’t always work this well. But such an all-weather absolute return approach using ETFs provides a lower-risk, easily-executable basis for participating in market upside while also offering protection – and hopefully profiting – during market downturns. And often you can profit even if the overall market stays flat. The key is to employ a relative ranking system that is generally predictive such that over time you can capture the cumulative performance spread between your baskets of long and short positions.

Scott Martindale is the Senior Managing Director for Sabrient Systems LLC (www.Sabrient.com) in Santa Barbara, CA. Sabrient publishes five quantitative indexes that are tracked by ETFs.

Click here to sign up for a free, online presentation by Larry Connors, CEO and founder of TradingMarkets, as he introduces The Machine, the first and only financial software that allows traders and investors to design and build quantified portfolios.