Here’s How to Find Top Performing Stocks Every Day

The question isn’t “Is the market efficient?” but

rather “How inefficient is the market?” and “How can we exploit this?” – Edward Thorp.

Over the many decades of academic studies and research done

by market professionals, nearly everything imaginable has been tested in an

attempt to predict the direction of a company’s stock price. P/E ratios,

dividend yield, revenue growth, book value, earnings growth, etc. have been

looked at over and over. The one conclusion that can be made from these studies

is that few, if any of them, show a real statistical edge. The one area which we

believe remains fertile ground for further research is price behavior.

Click here to order your copy of The VXX Trend Following Strategy today and be one of the very first traders to utilize these unique strategies. This guidebook will make you a better, more powerful trader.

What is price? It’s essentially a culmination of all the

known information of a company. Therefore, price is real as it represents what

the majority of the market participants know at that given time.

Finding Market Inefficiencies

Shorter-term, we believe that markets (prices) can be very

inefficient. We have published some of these inefficiencies over the years and

we’ll continue to publish them over time. Most of these short-term

inefficiencies tend to occur whenever there is either news in a stock, or there

is a great deal of fear in the market place. One only has to think about what

happened in the summer of 2007 to fully understand these inefficiencies. Solid

performing companies saw 20%, 30% and 40% of their value lost in a few days as

market participants (primarily institutions) irrationally sold stocks, only to see

the prices of many of these stocks quickly bounce back to their previous levels.

These types of market inefficiencies can be found on a regular basis in

individual stocks, especially on unexpected news-related events, or when market

volatility rises.

Longer-term, markets are supposedly more efficient. This is

the concept that has been taught by many in the academic world. But, if it

was true, you wouldn’t expect low volatility stocks to outperform high

volatility (and often times high beta stocks) by a better than 2-1 margin since

1995, would you? But they have…

How to Find Safe High Probability Stocks

Is it possible to increase your investment returns using

only price as an indicator? We believe the answer is yes, it is. And here’s how

you do it.

First, the one indicator that best measures the movement of

a stock (and based upon the statistics is the best indicator to predict a stocks

direction over the next year) is historical volatility.

What is historical volatility? Volatility is the annualized

standard deviation of daily returns (don’t get scared away…it gets simpler from

here). Simply stated, it’s the movement of a stock price without regard to

direction. Large average daily stock price changes (in percentage terms) mean

high volatility, and small average daily price changes mean low volatility.

Stated another way, the more a stock moves, the higher its volatility. The less

it moves, the lower its volatility.

Companies that are stable and are usually performing in-line with

expectations tend to have lower volatility (this is logical, as these companies

are more predictable). Companies that have a great deal of uncertainty to

them (think about the sub-prime lenders in 2007) tend to have higher

volatility as more is unknown.

Do You Invest High-Flying Stocks? Be Careful…

Now, the key thing to learn is that since 1995, high

volatility stocks have underperformed the market. In fact, on average, the majority has been

lower 252 trading days later.

On the other side of the equation, low volatility stocks have outperformed the market. And, on average, the

majority have been higher 252 trading days later.

Let’s look at the test that confirms this, and then we’ll look

at the results:

- We ran these test results from January 1, 1995 through May 31,

2007. - The universe of stocks we ran them on had a dynamic volume filter, to assure we were looking at the liquid stocks, and numbered

11,282 different stocks. - Survivorship bias has been omitted (meaning all

stocks that were public during this period of time were included in our

universe). - Trading costs were not included.

- We looked at every stock, every trading day. This means that we took the

universe of stocks each trading day, calculated their historical volatility

for that day and then looked at their performance 252 trading days (one-year)

later.

Each day we ranked the 100-day historical volatility of all

the stocks in our universe (we also tested using a 250-day HV and got similar

results, further showing the significance of these tests). We then compared the

252-day performance of the stocks which were in the top 20% of volatility (the

20% with the highest volatility) versus the 20% with the lowest volatility.

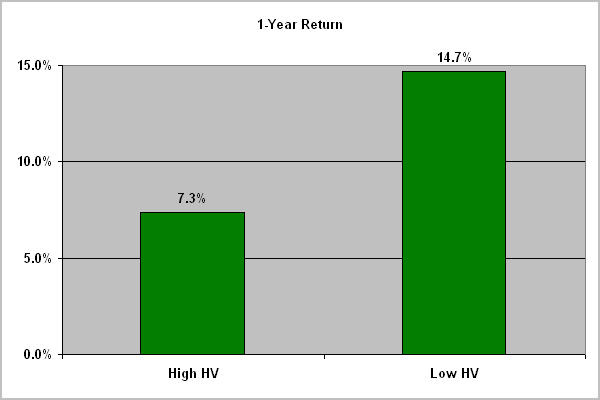

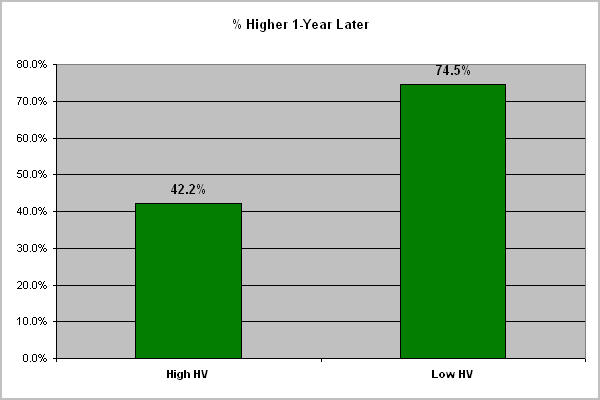

As you can see, the stocks in the lowest 20% ranked by

historical volatility outperformed the stocks with the highest volatility by a

better than 2-1 margin 252 days later. And the stocks with the lowest volatility

rose 74.5% of the time 252 days later, while the stocks with the highest

volatility rose only 42.2% of the time, a significant difference.

And

this difference gets even greater if you compare the lowest 10% with the highest

10%. For the lowest 10%, prices rose 77% of the time 252 days later, while the highest

10% rose only 39% of the time (meaning 61% of the time prices were lower 252

days later!).

One caveat to the above; the only time during the test

period this didn’t seem to hold true was in mid 1998-1999 when the internet

bubble was being formed. Money was chasing the high volatility stocks and many

of those stocks moved only in one direction. Therefore if you removed the bubble

period, the returns for the highest volatility stocks would be even worse. In

reality, as poor as the results have been for the most volatile stocks, they’d

be even worse without the 1998-99 bubble! This is something to think about

the next time you see or hear someone recommending some high-flying stock as the next sure

thing.

Summary

Trading high volatility stocks may be a

good idea if you are looking for short-term gains. But for investing, it appears

to be a recipe for underperformance and even potentially for disaster. We can

show you many high flying stocks with extreme volatility that collapsed in price over

the next twelve months. The safer and more prudent thing to do, is to identify

stocks with lower historical volatility readings. A 100-day historical

volatility reading under 30 is a good place to start. Since 1995, on average,

better than 70% of these stocks have been higher 252 days later. This is a

long-term track record that very few (if any) money managers and professionals

can come close to replicating.

We’ll continue to publish our research on this topic over

time. If you would like to see lists of stocks which incorporate the above

research, you can find them at www.PowerRatings.net.

Larry Connors is CEO and Founder of TradingMarkets.com and PowerRatings.net.

Cesar Alvarez is Managing Director of Connors Research LLC.